A Financial & Legal Guide

You’ve been wronged. You hire a lawyer, go to court, and win. Then you discover the other person has zero money, zero assets, and nothing in the bank. Winning felt great — until the reality hits: a court victory doesn’t automatically put money in your pocket.

So, what happens if you sue someone with no money? The short answer is that you can win the case, but collecting is a completely different battle. This guide walks you through every step — from what “judgment proof” actually means, to the legal tools you can use to collect years from now.

Can You Sue Someone With No Money?

The Short Answer: Yes — But Here’s the Catch

Yes, you can legally sue someone with no money and win a judgment against them. Nothing in U.S. law requires a defendant to have money before you file a lawsuit. However, winning the case makes you a Judgment Creditor — meaning the court officially says they owe you. The problem? If they truly have nothing, they are considered “judgment proof,” and the court cannot force them to produce money they simply do not have.

Think of it this way: a court ruling is like a permission slip to collect. It doesn’t generate cash on its own.

What Does It Mean to Be Judgment Proof?

Defining the Judgment Debtor Ecosystem

When you win a civil lawsuit, your legal title changes. You become the Judgment Creditor (the one owed money). The losing party becomes the Judgment Debtor (the one who owes). If the Judgment Debtor has no liquid funds, no real estate equity, and no seizable property, courts and attorneys describe them as judgment proof.

Important nuance: “Judgment proof” is not an official legal status. It is a practical description of someone whose income and assets fall so far below collection thresholds — or are so well protected by law — that no enforcement tool can reach them right now.

The key phrase is “right now.” A debtor’s financial situation can change. That’s where long-term strategy comes in (more on that below).

How Do Lawyers Find Out If Someone Has Money Before Suing?

The Mechanics of a Pre-Litigation Asset Search

Before filing a lawsuit, experienced litigation attorneys run a pre-litigation asset search to determine whether suing is even worth the expense. Here’s how they do it:

- LexisNexis & Westlaw databases — These proprietary research platforms aggregate public records across counties, states, and federal courts. Attorneys use them to scan for property ownership, business interests, UCC filings, and prior judgments.

- Secretary of State (SOS) corporate records — If the person owns a business, SOS filings reveal LLC ownership, registered agents, and business assets.

- County real estate deeds — Property records show whether the debtor owns a home or land and what liens already exist against it.

- Vehicle title searches — DMV records reveal registered vehicles, which can be seized under certain conditions.

- Credit header data — Basic information like address history and employer data can point to garnishable income sources.

A thorough asset search typically costs $150–$500 and can save thousands in wasted legal fees. Some plaintiff’s attorneys offer contingency arrangements (no fee unless you collect) precisely because they run this analysis first.

[INSERT IMAGE HERE: A magnifying glass hovering over a digital map of property records and financial data charts. Alt Text: Pre-litigation asset search tools used by attorneys to find debtor assets Title Text: How Lawyers Search for Debtor Assets Before a Lawsuit Caption: A professional asset search uses multiple public record databases. AI Generation Prompt: Clean editorial illustration: a large magnifying glass over a stylized digital dashboard showing icons for a house, a car, a bank, and corporate paperwork. Dark green and lime green color palette. No faces. No text. 1200×800 px, WebP quality 82%.]

What Asset Exemptions Protect a Debtor’s Money and Property?

Understanding Statutory Exemptions and Protected Income

Even if you win your lawsuit, the law draws a clear line: creditors cannot strip a debtor of their basic livelihood. Federal and state statutes protect certain income streams and assets entirely. These are called exempt assets, and seizing them is illegal regardless of what your court judgment says.

Navigating Wage Garnishment Limits in 2026

Wage garnishment is one of the most common collection tools. But federal law under the Consumer Credit Protection Act (CCPA) caps how much can be taken:

- Maximum garnishment: The lesser of 25% of disposable weekly earnings, or the amount by which weekly earnings exceed 30 times the federal minimum wage ($7.25/hr × 30 = $217.50/week protected).

- Example: If your debtor earns $600/week after taxes, a creditor can garnish up to $150/week (25% of $600). But if they earn only $250/week, only $32.50 can be taken ($250 − $217.50), leaving them nearly untouched.

- Child support and alimony: These are different — creditors can garnish up to 50–60% of disposable earnings for family support obligations.

- Four states prohibit consumer wage garnishment entirely: Texas, Pennsylvania, North Carolina, and South Carolina do not allow wage garnishment for ordinary consumer debts, though bank account levies may still apply.

Fully Protected Income Streams (100% exempt under federal law):

- Social Security benefits (SSI and retirement)

- Veterans Administration (VA) benefits

- Civil service and federal retirement payments

- Supplemental Security Income (SSI)

- Unemployment compensation (in most states)

- Workers’ compensation benefits

The 2026 Homestead Exemption and Bankruptcy Court Shield

The homestead exemption protects equity in a debtor’s primary residence. Here’s what the 2026 numbers look like:

| Jurisdiction | 2026 Homestead Exemption |

|---|---|

| Federal (11 U.S.C. § 522(d)(1)) | $31,575 per person / $63,150 married |

| Maryland | Tied to federal cap ($31,575) |

| Georgia | $21,500 individual / $43,000 married (standard) |

| Texas | Unlimited (subject to 40-month residency rule) |

| Florida | Unlimited on acreage; restrictions on new purchases |

Source: 11 U.S.C. § 522 (Federal Register, April 1, 2025 triennial adjustment, valid through March 31, 2028)

What this means in plain English: If a debtor owns a home with $30,000 in equity and they’re in a state that follows the federal exemption, that entire amount is off-limits to you as a creditor. You cannot force a sale of their house to collect your judgment.

How Do You Collect Money From a Judgment Proof Debtor?

Activating Your Post-Judgment Collection Toolkit

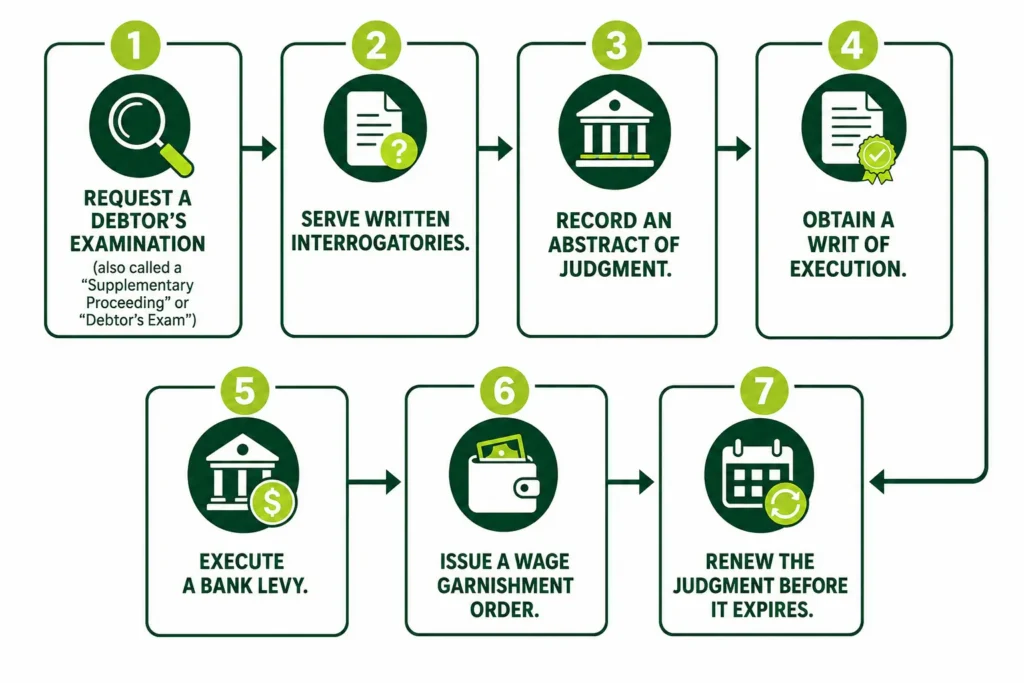

Winning your lawsuit is Step 1. Collecting is Steps 2 through 20. Here is the formal execution process most attorneys follow:

Forcing Transparency via Supplementary Proceedings

Before you can seize anything, you need to know exactly what exists to seize.

Step 1: Request a Debtor’s Examination (also called a “Supplementary Proceeding” or “Debtor’s Exam”). File a motion with the court to compel the judgment debtor to appear and answer questions under oath about their income, assets, bank accounts, property, and business interests. This is the discovery phase of collection. If they lie, they risk contempt of court charges.

Step 2: Serve Written Interrogatories. In some states, you can mail written questions (interrogatories) requiring the debtor to disclose all financial accounts, employer information, and property holdings without a formal court appearance.

Recording an Abstract of Judgment with the County Recorder

Step 3: Record an Abstract of Judgment. Once you have a judgment, file an Abstract of Judgment with the County Recorder’s Office in every county where the debtor owns (or may own) real property. This creates an automatic judgment lien on any real property the debtor currently owns or acquires in the future in that county.

This is a critical step. Even if the debtor is broke today, if they buy a house tomorrow, your lien attaches immediately — and they cannot sell or refinance without paying you first.

Deploying a Writ of Execution to the Sheriff’s Department

Step 4: Obtain a Writ of Execution. A writ of execution is a court order directing the sheriff to seize non-exempt assets. File it with the court clerk and then serve it on the appropriate party (the debtor’s bank, employer, or the sheriff).

Step 5: Execute a Bank Levy. Direct the sheriff or levying officer to serve the writ on the debtor’s financial institution. The bank must freeze and turn over non-exempt funds in the account.

Step 6: Issue a Wage Garnishment Order. If the debtor is employed, serve the writ on their employer. The employer must withhold the legally allowable percentage from each paycheck and send it directly to the court or to you.

Step 7: Renew the Judgment Before It Expires. In most states, judgments last 10 years (California, New York) or 20 years (some states). You can often renew them. Never let your judgment expire before you’ve collected — renewing is far cheaper than re-litigating.

What Is the “Asset Horizon” Strategy in Litigation?

Playing the Long Game Against Post-Judgment Interest

Here’s a concept most articles on this topic completely ignore: the Asset Horizon.

The Asset Horizon is a long-term collection framework. It works like this: instead of writing off a judgment against a broke debtor, you analyze their future earning potential — their career trajectory, education level, industry, and age — and calculate whether waiting 5, 10, or 20 years makes financial sense.

Why does this work? Because your judgment doesn’t sit still. It accrues interest.

- Federal civil judgments accrue interest tied to the 1-year Treasury yield (roughly 3.70–3.80% in mid-2026, per 28 U.S.C. § 1961).

- Many state courts set higher rates. Florida, for example, has set rates above 8% in certain periods.

- Some states like Utah calculate post-judgment interest at the federal rate plus 2%.

Example of the Asset Horizon in action:

| Year | Original Judgment | Accrued Interest (at 5% avg) | Total Owed |

|---|---|---|---|

| 2026 (today) | $50,000 | $0 | $50,000 |

| 2031 (5 years) | $50,000 | ~$13,814 | ~$63,814 |

| 2036 (10 years) | $50,000 | ~$31,445 | ~$81,445 |

| 2046 (20 years) | $50,000 | ~$82,759 | ~$132,759 |

A 25-year-old debtor who’s broke today may be a mid-career professional earning six figures by 2036. Your judgment — and that Abstract of Judgment on file — is still waiting for them.

Can a Judgment Debtor Wipe Out Your Lawsuit in Bankruptcy?

Understanding Chapter 7 vs. Chapter 13 Automatic Stays

This is the nightmare scenario for creditors. The moment a debtor files for bankruptcy, an automatic stay kicks in under 11 U.S.C. § 362. This immediately freezes all collection efforts — your garnishments stop, your bank levy is suspended, and court proceedings halt.

- Chapter 7 bankruptcy (liquidation): The debtor’s non-exempt assets are sold by a trustee to pay creditors. Most unsecured debts, including civil judgments, are discharged (wiped clean). You may receive cents on the dollar — or nothing.

- Chapter 13 bankruptcy (repayment plan): The debtor proposes a 3–5 year repayment plan. You may receive partial payment, but the automatic stay still blocks immediate collection.

The Loophole: Non-Dischargeable Debt and Intentional Torts

Not every judgment can be erased in bankruptcy. The Bankruptcy Code (11 U.S.C. § 523) lists categories of non-dischargeable debt — obligations that survive bankruptcy no matter what:

- Debts from willful and malicious injury (intentional assault, fraud, conversion of property)

- Debts from fraudulent misrepresentation

- Child support and alimony arrears

- Fines and restitution from criminal convictions

- Student loans (with limited hardship exceptions)

Practical example: If someone deliberately destroyed your property or defrauded you out of money, that judgment likely survives their bankruptcy filing. You’ll need to file an adversary proceeding inside the bankruptcy case to preserve your claim — a lawsuit within a lawsuit, essentially. An attorney is essential here.

Does Insurance Cover a Lawsuit If the Person Has No Money?

Uncovering Third-Party Liability and Indemnification

Before giving up on a broke defendant, always ask one question: Is there an insurance policy in play?

Individuals may be personally broke, but their insurance carrier could be sitting on a substantial payout. Common scenarios:

- Auto accident: Even a judgment-proof driver likely carries auto liability insurance. Your claim shifts from the driver to their insurer, which has actual assets.

- Homeowner or renter’s insurance: Property damage or personal injury incidents on someone’s property may be covered under their homeowner’s or renter’s policy.

- Employer liability (respondeat superior): If the defendant was acting within the scope of their employment when they harmed you, their employer’s commercial general liability (CGL) insurance may cover the claim — and employers typically have much deeper pockets.

- Umbrella policies: Wealthy-appearing-but-liquid-poor individuals sometimes carry personal umbrella policies ($1M+) that activate when other coverage is exhausted.

Always subpoena insurance declaration pages during discovery. Attorneys routinely use this to pivot an otherwise hopeless case toward a fully insured corporate defendant.

Case Study & Financial Calculation: The Real Cost of Suing

Does It Actually Pay Off?

Let’s run the numbers on a realistic scenario. You’re owed $25,000 by someone with no money. You hire an attorney on an hourly basis.

| Expense | Estimated Cost |

|---|---|

| Attorney fees (30 hrs × $350/hr) | $10,500 |

| Court filing fees | $450 |

| Pre-litigation asset search | $350 |

| Process server fees | $150 |

| Sheriff’s levy fee | $200 |

| Abstract of Judgment filing | $75 |

| Total spent | $11,725 |

Now assume you collect $8,000 through wage garnishment over 18 months (debtor earns $500/week after taxes, $70.63/week garnished).

Net recovery: $8,000 − $11,725 = negative $3,725.

You lost money. This is why the pre-litigation asset search and contingency fee agreements matter so much. If an attorney doesn’t believe you’ll collect, they won’t take it on contingency — which is itself a signal about whether suing makes financial sense.

Pros and Cons: Contingency Fee vs. Hourly Legal Billing

Which Fee Structure Is Right for Your Case?

| Contingency Fee | Hourly Retainer | |

|---|---|---|

| How it works | Attorney takes 25–40% of what you collect. No win, no fee. | You pay by the hour, win or lose. |

| Upfront cost | $0 (or minimal filing fees) | $3,000–$15,000+ retainer up front |

| Risk | Attorney absorbs litigation risk | You absorb all financial risk |

| Best for | Cases with clear liability AND collectible defendant | Cases with complex legal issues or institutional defendants |

| Watch out for | Attorney may drop case if collection looks impossible | Meter keeps running even if debtor is broke |

| Ideal scenario | Personal injury, insurance-backed claims, clear assets | Business disputes, contract cases, fraud with traceable assets |

Bottom line: Contingency is usually better when chasing individuals. Hourly billing is worth it when you know there are assets to find.

Frequently Asked Questions (FAQ)

Can you go to jail if you lose a lawsuit and can’t pay?

No. The United States abolished debtors’ prisons in the 19th century. Losing a civil lawsuit and being unable to pay will not result in jail time. However, if a judge orders you to appear for a debtor’s examination and you willfully refuse to appear, you can be held in contempt of court, which can carry fines or, in rare cases, brief incarceration.

How long does a court-ordered judgment last?

It depends on the state. Most states allow judgments to remain valid for 10 years (including California, New York, and Florida), while others allow 20 years. Creditors can typically renew a judgment before it expires for an additional term. Always docket your renewal deadline — a lapsed judgment cannot be enforced.

Can a creditor freeze a joint bank account?

Yes, in most states. A bank levy can freeze the entire joint account, even if only one account holder is the judgment debtor. The non-debtor account holder must then file a claim of exemption to recover their portion of the funds. The Fair Debt Collection Practices Act (FDCPA) and the Consumer Financial Protection Bureau (CFPB) provide some protections, but joint account risk is real and often surprises co-owners.

What happens if a judgment debtor hides assets?

Concealing assets from creditors during a debtor’s examination is perjury — a criminal offense. Courts take this seriously. If discovered, the debtor can face contempt charges, criminal referral, and adverse inferences in court. Additionally, the Uniform Fraudulent Transfer Act (UFTA) — now updated to the Uniform Voidable Transactions Act (UVTA) in many states — allows creditors to unwind transfers made to hide assets up to 4–7 years prior. Transfers to family members or related parties right before a lawsuit are red flags courts scrutinize closely.

Conclusion: Is Suing a Broke Person Worth It?

Suing someone with no money is legally possible but financially risky. You can win. You can get a judgment. But turning that judgment into actual cash requires patience, legal tools, and sometimes years of waiting.

Here’s the framework to decide:

- Run an asset search first. Know what you’re working with before spending a dollar on litigation.

- Check for insurance. A broke defendant with an insurance policy is not truly broke — their insurer is the real target.

- Think long-term. An Abstract of Judgment filed today attaches to property they buy in 10 years. Post-judgment interest keeps the clock running in your favor.

- Consider settlement. A partial settlement today may beat a full judgment that never gets paid.

- Work with a contingency attorney. If no attorney will take your case on contingency, that’s a data point about collectibility.

The law gives creditors real tools. The Asset Horizon strategy, judgment liens, wage garnishment, and bank levies all work — but only when there’s something to reach. The best move is to know your target’s financial reality before pulling the trigger on litigation.

Next step: Consult a collections attorney in your state for a free or low-cost case evaluation. Many offer 30-minute consultations to review your judgment and assess collectibility. This article is educational, not legal advice.

References

- Consumer Credit Protection Act (CCPA), 15 U.S.C. § 1671 et seq. — dol.gov/agencies/whd/garnishment (rel=”noopener” target=”_blank”)

- 11 U.S.C. § 522 — Federal Bankruptcy Exemptions (2025–2028 triennial adjustment) — law.cornell.edu/uscode/text/11/522 (rel=”noopener” target=”_blank”)

- 28 U.S.C. § 1961 — Post-Judgment Interest Rate — uscourts.gov/court-programs/fees/post-judgment-interest-rate (rel=”noopener” target=”_blank”)

- Consumer Financial Protection Bureau (CFPB) — Wage Garnishment Explainer — consumerfinance.gov (rel=”noopener” target=”_blank”)

- Nolo Legal Encyclopedia — Federal Bankruptcy Exemptions 2025–2028 — nolo.com (rel=”noopener” target=”_blank”)

By

By