Cash App Afterpay integrates Buy Now, Pay Later functionality directly into the Cash App interface. Cash App Afterpay allows users to split online checkouts, finance physical purchases, and convert peer-to-peer transfers into short-term installment loans.

If you are wondering how does cash app afterpay work, the answer changed significantly in 2026. The platform shifted from a basic retail checkout tool into a complete digital lending ecosystem. You no longer need to switch between different apps to manage your spending. Block, Inc., the parent company, merged these tools to give users ultimate flexibility over their cash flow.

Today, Cash App Afterpay lets you swipe a physical debit card for groceries, send rent money to a roommate, or buy clothes online. You can then retroactively chop those expenses into manageable weekly payments. This guide breaks down the exact math, the hidden fees, and the specific rules governing this new financial ecosystem.

What Is the Afterpay on Cash App Card Feature?

The Afterpay on Cash App Card feature represents a digital lending mechanism that allows users to finance real-world physical transactions. The Afterpay on Cash App Card feature converts standard debit card swipes into short-term loans directly at the point of sale.

Before this update, consumers could only use Buy Now, Pay Later (BNPL) at participating online retailers. Now, if you have a physical card, you can shop anywhere. You simply make a purchase over $25 using your card. Then, you open your activity tab and select the option to pay over time. The app instantly refunds the purchase amount to your balance. It then creates an active installment loan that you pay back over several weeks.

Leveraging the Visa Network for Everyday Purchases

The Visa Network operates as the global payment processing infrastructure that facilitates these transactions. By utilizing the Visa Network, Cash App cardholders can finance everyday purchases at any physical terminal that accepts standard credit card payments.

This is a massive shift. You are no longer restricted to brand partners like Levi’s or Sephora. Because the physical card runs on the Visa Network, you can buy gas, pay a medical bill, or handle emergency car repairs. The system treats the swipe just like a standard purchase. Afterward, you use the app to break that specific transaction into a customized payment plan.

How Can Users Access Peer-to-Peer (P2P) Financing?

Peer-to-Peer (P2P) Financing constitutes a lending service that allows users to retroactively convert personal money transfers into manageable payment plans. Peer-to-Peer (P2P) Financing provides users the ability to send immediate funds to friends or family while repaying the sent amount over several weeks.

Historically, BNPL only applied to retail merchants. In 2026, Cash App changed the game. You can now finance the money you send directly to other people. If you need to split a $200 dinner bill or pay your half of the utilities, you can send the money immediately. Later, you simply tap the transaction and convert it into a loan. This keeps your immediate cash reserves high while spreading the financial burden over time.

Converting a $Cashtag Transfer into an Installment Loan

A $Cashtag functions as the unique identifier required to execute seamless money transfers within the platform. Users select a recent $Cashtag transfer over $25 to immediately convert the completed transaction into an active installment loan.

To understand how does cash app afterpay work for personal transfers, look at your recent activity. As long as you used your linked Cash App Card to fund the transfer within the last 7 days, you will see a “Pay over time available” button next to the $Cashtag. Tapping this button instantly generates a loan agreement. It refunds the cash to your available balance and schedules your future payments automatically.

Case Study: How Is the 7.5% Finance Fee and Repayment Hierarchy Calculated?

A calculation case study models the exact mathematical costs associated with securing a short-term consumer loan. This calculation case study demonstrates how the platform applies a flat 7.5% Finance Fee and schedules automatic deductions based on a strict Repayment Hierarchy.

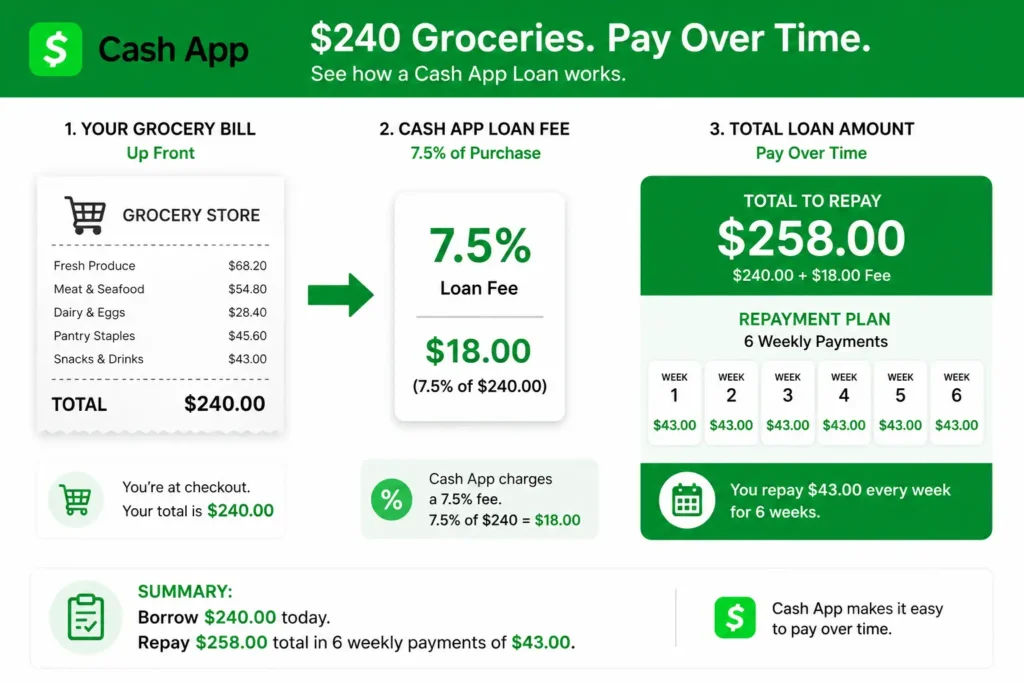

Let’s look at a practical example. Imagine you spend $240 on groceries using your Cash App Card. You decide to convert this into a 6-week loan. Unlike traditional retail Afterpay, converting past purchases carries a flat fee.

- The Principal: $240.00

- The 7.5% Finance Fee: $18.00

- Total Loan Amount: $258.00

You must repay this $258 over six weeks. This usually results in six weekly payments of $43.00. When a payment comes due, the platform uses a strict Repayment Hierarchy. It pulls the $43 from your Cash App balance first. If your balance is empty, it automatically charges the debit card or bank account you linked to the app.

Understanding the 65.15% Fixed APR Under the Truth in Lending Act (TILA)

The Truth in Lending Act (TILA) exists as a federal mandate requiring lenders to disclose the true cost of borrowing. Under the Truth in Lending Act, the standard 7.5% fee equates to a 65.15% Fixed APR when applied to a standard 42-day loan cycle.

An Annual Percentage Rate (APR) measures the yearly cost of borrowing money. While a 7.5% flat fee sounds small, the timeline matters. Because you must pay the loan back in just 6 weeks (42 days), the annualized cost of that debt is mathematically steep. The Truth in Lending Act (TILA) forces lenders to show this exact 65.15% Fixed APR before you tap “accept.” You must always review these disclosures.

How Does Real-Time Data Underwriting Compare to a FICO® Score?

Real-Time Data Underwriting evaluates a borrower’s immediate cash flow and direct deposit history to determine lending eligibility. Real-Time Data Underwriting replaces the backward-looking FICO® Score by analyzing the user’s active financial behavior within The Block Ecosystem.

Traditional banks rely heavily on your FICO® Score to approve loans. This three-digit number looks at years of past credit history. Cash App takes a modern approach. The algorithm analyzes how much money you receive in direct deposits, how often you use your debit card, and how quickly you pay friends. If your cash flow is healthy, you can qualify for Cash App Afterpay even if your traditional credit score is low.

The Soft Credit Inquiry vs. The Block Ecosystem Cash Flow Assessment

A Soft Credit Inquiry allows lenders to review a consumer’s credit report without negatively impacting the consumer’s official credit rating. The Block Ecosystem combines a Soft Credit Inquiry with an internal cash flow assessment to underwrite users who lack traditional credit histories.

When you apply, the app performs a Soft Credit Inquiry. This verifies your identity and checks for major red flags like bankruptcies. However, it does not lower your credit score. The real decision happens inside The Block Ecosystem. The algorithm trusts the money it can actually see flowing through your account today, rather than a missed credit card payment from five years ago.

What Are the Options for the Pay-in-4 Model vs. Pay Monthly Long-Term Installments?

The Pay-in-4 Model splits a retail purchase into four equal payments spread over six weeks without charging interest. In contrast to the Pay-in-4 Model, Pay Monthly / Long-Term Installments allow users to finance larger purchases over 3, 6, 12, or 24 months with a standard interest rate attached.

If you shop online at a partnered retailer, the classic Pay-in-4 Model remains zero-interest. You pay 25% at checkout and make three more payments every two weeks. However, for major purchases ranging from $100 up to $4,000, you need longer terms. Cash App offers Pay Monthly plans. These longer-term loans do carry interest, but they make expensive items like laptops or furniture immediately affordable.

Buy Now, Pay Later (BNPL) Limits and the Role of First Electronic Bank

Buy Now, Pay Later (BNPL) limits establish the maximum dollar amount a consumer can borrow for a single transaction. First Electronic Bank officially originates all Buy Now, Pay Later loans, ensuring the financial products comply with state and federal lending regulations.

Cash App does not actually lend you the money itself. First Electronic Bank is the legal entity that funds these loans. They set strict Buy Now, Pay Later (BNPL) limits based on your profile. A beginner might only get a $100 limit. However, as you successfully repay loans on time, the system automatically increases your purchasing power.

How Do Cash App BNPL Options Compare for Daily Spending? (Pros & Cons)

A comparison of lending options helps consumers evaluate the financial risks and benefits associated with financing daily expenses. This daily spending comparison highlights the dangers of financing groceries against the convenience of zero-interest retail loans.

When evaluating how does cash app afterpay work for your lifestyle, you must weigh the convenience against the costs. Financing a winter coat at 0% interest is smart. Paying a 65.15% APR to finance your weekly groceries is a financial trap.

Pros of Cash App Afterpay:

- Zero-Interest Retail: Standard online Pay-in-4 checkouts remain completely free if paid on time.

- Universal Access: The physical card allows you to finance purchases anywhere Visa is accepted.

- No Credit Damage: The application relies on soft credit checks and internal cash flow data.

- Emergency Liquidity: Retroactive P2P financing helps you survive sudden cash shortages.

Cons of Cash App Afterpay:

- High Effective APR: The 7.5% flat fee on physical swipes mathematically equals a 65.15% APR.

- Strict Auto-Payments: The system automatically drafts money from your accounts without asking.

- Debt Cycle Risk: Financing daily consumables (like gas or groceries) can quickly trap users in a cycle of debt.

Security Protections from the Federal Deposit Insurance Corporation (FDIC) and Consumer Financial Protection Bureau (CFPB)

The Federal Deposit Insurance Corporation (FDIC) insures consumer deposits held within partner banking institutions. The Consumer Financial Protection Bureau (CFPB) actively monitors these lending products to ensure borrowers receive fair treatment regarding late fees and dispute resolutions.

Your money is safe inside the app. If you have a sponsored Cash App Card, your funds benefit from pass-through insurance via the Federal Deposit Insurance Corporation (FDIC). Furthermore, the Consumer Financial Protection Bureau (CFPB) regulates how these loans operate. If you encounter unfair late fees or billing errors, federal law guarantees your right to dispute the charges and seek immediate resolution.

Frequently Asked Questions (FAQ) About Cash App Loans Administered by Square Capital, Inc.

Frequently Asked Questions clarify the operational rules and user restrictions regarding digital installment loans. Frequently Asked Questions explain exactly how Square Capital, Inc. services the active loan portfolios and manages consumer payment schedules.

Do I need a separate Afterpay account to use the feature?

No, you do not need a separate account. If you sign up directly through Cash App, all loan management, payment scheduling, and customer support happen entirely within the Cash App interface. The integration is fully native.

Does Afterpay on Cash App check your credit?

Yes, but it only performs a soft credit check. This soft pull verifies your identity and basic creditworthiness, but it will not appear as a hard inquiry on your official credit report and will not lower your FICO® Score.

What is the spending limit for Afterpay on Cash App?

Limits are entirely personalized based on your app usage and cash flow. For standard short-term loans, limits typically range from $25 up to $1,000. For longer-term monthly installment plans, eligible users can finance up to $4,000. Your limit increases as you build a positive repayment history.

By

By