A mortgage qualification limit defines the exact dollar amount a financial institution will lend a homebuyer. It depends on a strict evaluation of your gross monthly income, credit health, and recurring monthly debt obligations — not just what you think you can afford.

Most people start their home search backward: they fall in love with a house, then try to figure out if they qualify. A smarter move? Learn your number first. This guide walks you through every factor lenders use in 2026 — in plain English, with real examples.

What Is the Maximum Mortgage You Can Qualify For?

The maximum mortgage you can qualify for is the highest principal loan balance an underwriter will approve. Think of the underwriter as a financial gatekeeper — their job is to confirm you can repay the loan without defaulting.

Underwriters calculate your maximum by applying the 28/36 rule:

- 28% — No more than 28% of your gross monthly income should go toward housing costs.

- 36% — No more than 36% should cover all debts combined (housing + car + student loans + credit cards).

Quick example: If you earn $7,000 per month before taxes, your maximum housing payment should stay at or below $1,960 (28%), and your total debt payments at or below $2,520 (36%).

Simple enough, right? But there’s more to it. Several additional metrics — DTI ratio, FICO® score, and loan type — all shift your final number up or down.

Calculating the Front-End and Back-End Debt-to-Income Ratio (DTI)

The Debt-to-Income Ratio (DTI) measures what percentage of your gross monthly income goes toward debt payments. It is the single most powerful number in mortgage underwriting.

There are two types:

Front-End DTI — housing expenses only (mortgage payment, property tax, homeowners insurance, HOA fees) Back-End DTI — housing expenses plus all recurring monthly debts (car loans, student loans, credit cards, personal loans)

| Loan Type | Max Front-End DTI | Max Back-End DTI |

|---|---|---|

| Conventional (Fannie Mae) | 28% | 36–50% (with compensating factors) |

| FHA | 31% | 43–57% (with compensating factors) |

| VA | No hard cap | 41% benchmark (residual income applies) |

| USDA | 29% | 41–46% |

| Jumbo | 28% | 43% (strict) |

Pro tip: Most lenders in 2026 prefer a back-end DTI of 43% or below for the best approval odds, regardless of loan type.

Real math example:

Suppose Maria earns $6,500/month gross. She has a $400/month car payment and $200/month in student loan payments.

- Total existing debts: $600/month

- Back-end DTI budget at 43%: 43% × $6,500 = $2,795/month

- Maximum housing payment (PITIA): $2,795 − $600 = $2,195/month

That $2,195 is Maria’s ceiling — before lenders even look at her credit score.

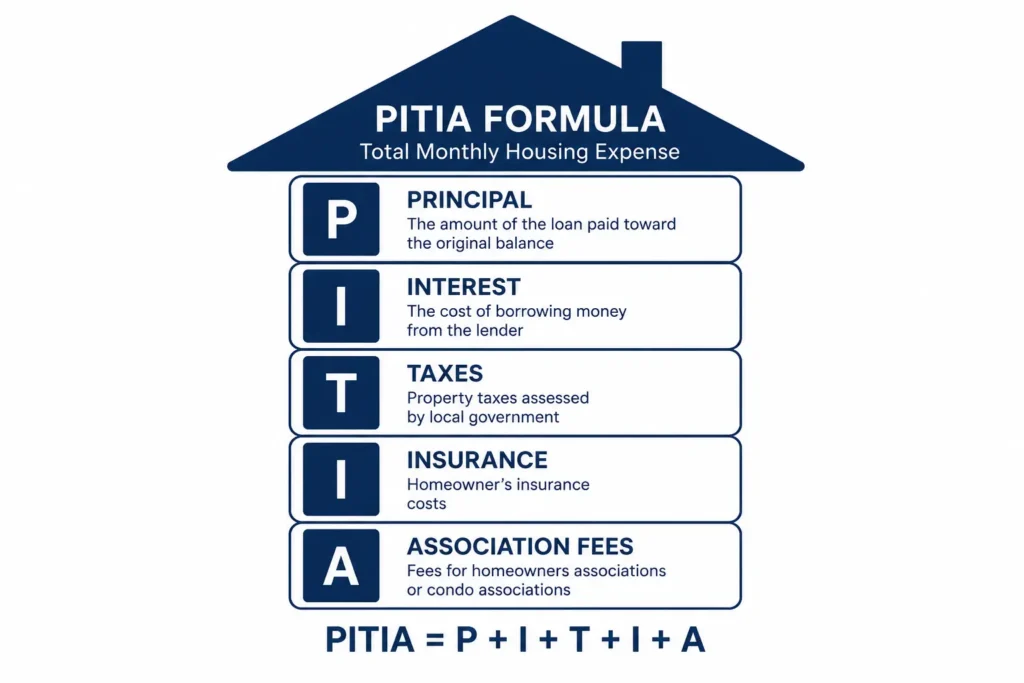

How Does the PITIA Formula Determine Your Borrowing Power?

The PITIA formula is the exact calculation underwriters use to measure your total monthly housing expense. It stands for:

- P — Principal (the loan amount you’re repaying)

- I — Interest (the lender’s fee for lending the money)

- T — Property Taxes (paid monthly into escrow)

- I — Insurance (homeowners insurance, also escrowed)

- A — Association Fees (HOA dues, if applicable)

Most mortgage calculators only show you principal + interest. That’s incomplete. Your actual monthly payment will almost always be higher once taxes, insurance, and HOA fees are added.

Example: A $400,000 home purchase with 10% down in a mid-range market might look like this:

| PITIA Component | Estimated Monthly Cost |

|---|---|

| Principal + Interest (at 6.8%, 30-yr) | $2,353 |

| Property Tax (1.2% annually) | $400 |

| Homeowners Insurance | $120 |

| PMI (if <20% down) | $150 |

| HOA Fees | $100 |

| Total PITIA | $3,123 |

To afford this payment under the 28% front-end rule, you’d need a gross monthly income of at least $11,154 — or roughly $133,800/year.

The Impact of Your FICO® Score and Loan-to-Value Ratio (LTV)

Your FICO® Score and Loan-to-Value Ratio (LTV) are the two primary risk metrics every lender runs before quoting you a rate.

FICO® Score

The FICO® Score (registered trademark of Fair Isaac Corporation) ranges from 300 to 850. A higher score means lower perceived risk — and a lower interest rate for you.

| FICO® Score Range | Typical Mortgage Impact |

|---|---|

| 760–850 | Best rates available; easier approval |

| 700–759 | Good rates; standard approval |

| 660–699 | Moderate rates; may need compensating factors |

| 620–659 | FHA eligible; higher rates; stricter scrutiny |

| 580–619 | FHA with 10% down only; very limited conventional options |

| Below 580 | Most lenders decline; manual review required |

Even a 0.5% rate difference can cost (or save) you tens of thousands over a 30-year loan. On a $350,000 mortgage, the difference between a 6.5% and a 7.0% rate is roughly $115/month — or $41,400 over the life of the loan.

Loan-to-Value Ratio (LTV)

The LTV measures how much of the home’s value you’re borrowing. The formula:

LTV = Loan Amount ÷ Appraised Home Value × 100

For a $400,000 home with a $40,000 down payment (10%):

LTV = $360,000 ÷ $400,000 = 90%

A lower LTV means less risk for the lender — which typically means better rates and no mandatory Private Mortgage Insurance (PMI). Most conventional lenders drop PMI once your LTV reaches 80% (20% equity).

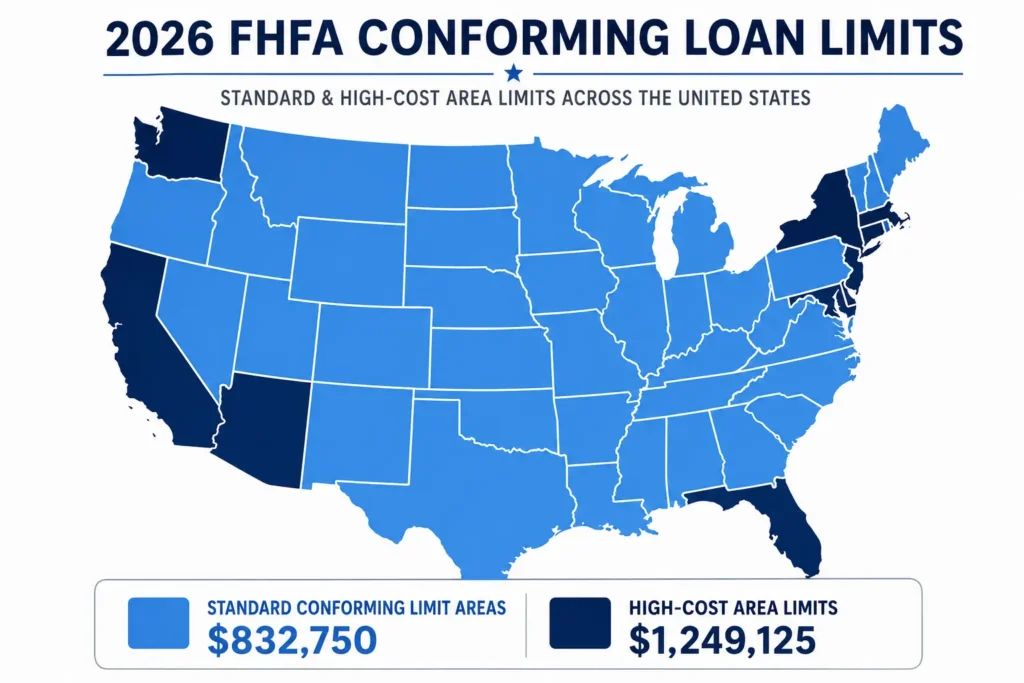

What Are the 2026 FHFA Conforming Loan Limits?

The Federal Housing Finance Agency (FHFA) sets annual conforming loan limits — the maximum mortgage size that Fannie Mae and Freddie Mac will purchase and guarantee.

For 2026, the FHFA raised the baseline conforming loan limit by 3.26%, reflecting the increase in average U.S. home prices:

| Property Type | 2025 Limit | 2026 Limit | Change |

|---|---|---|---|

| 1-unit (single-family) | $806,500 | $832,750 | +$26,250 |

| 2-unit | $1,032,650 | $1,066,350 | +$33,700 |

| 3-unit | $1,248,150 | $1,288,850 | +$40,700 |

| 4-unit | $1,551,250 | $1,601,750 | +$50,500 |

High-cost areas (think: San Francisco, New York City, Seattle) have a ceiling of $1,249,125 for single-family homes. Special territories like Alaska, Hawaii, Guam, and the U.S. Virgin Islands reach $1,873,675.

Why does this matter? If your loan stays under the conforming limit, you qualify for standard Fannie Mae or Freddie Mac backing — which typically means lower rates and easier approval. Go above that line, and you’re in jumbo mortgage territory.

Fannie Mae (FNMA) Standard Mortgages vs. Jumbo Mortgages

Fannie Mae (FNMA) standard mortgages stay within the FHFA conforming limits and follow federal underwriting guidelines. They’re widely available, competitively priced, and accessible to most borrowers with decent credit.

Jumbo Mortgages exceed the conforming loan limit ($832,750 in most areas for 2026). Because Fannie Mae and Freddie Mac won’t buy these loans, lenders hold them on their own books — meaning stricter requirements:

- Typically require FICO® 700+ (many lenders require 720+)

- Back-end DTI usually capped at 43% — no exceptions

- Down payment often 10–20% minimum

- 12–18 months of cash reserves commonly required

If you’re buying in an expensive market and need a jumbo loan, budget extra time for underwriting. The documentation bar is higher.

How Do Self-Employed Buyers Qualify with Schedule C and 1099 Income?

Self-employed borrowers — freelancers, independent contractors, small business owners, digital entrepreneurs — face a uniquely tricky qualification path. Why? Because lenders don’t use your gross revenue. They use your net profit.

Here’s how it works:

For sole proprietors (Schedule C filers): Lenders average the net profit from your last two years of federal tax returns. They add back certain non-cash deductions (like depreciation) to determine your “qualifying income.”

For 1099 contractors: Lenders average your 1099 income over 24 months. Inconsistent year-over-year income can be a red flag.

Common stumbling block: If you aggressively write off business expenses (reducing your taxable income), your qualifying income will also be lower. That can shrink your loan eligibility significantly.

Documents you’ll need:

- Two years of personal federal tax returns (with all schedules)

- Two years of business tax returns (if incorporated)

- Year-to-date Profit & Loss statement

- 12 months of business bank statements (many lenders now accept bank statement programs as an alternative)

Example: David runs a web design business. His 2024 Schedule C shows $90,000 in gross revenue but $50,000 in net profit after deductions. His 2025 net profit was $62,000. Lenders average these to $56,000/year — or $4,667/month — as his qualifying income, regardless of what his business actually deposited.

Alternative Option: Debt Service Coverage Ratio (DSCR) Loans

If you’re purchasing an investment property (not a primary residence), there’s a separate path: Debt Service Coverage Ratio (DSCR) lending.

DSCR lenders evaluate whether the property’s rental income can cover the mortgage payment — your personal income is secondary or even irrelevant.

DSCR Formula: Monthly Rental Income ÷ Monthly PITIA

A DSCR of 1.25 or higher is typically required — meaning the property generates at least $1.25 in rental income for every $1.00 in mortgage payment. Real estate investors love DSCR loans precisely because they sidestep traditional income verification.

Case Study: The 2026 AUS Stress Test — $80,000/Year Salary

Let’s put it all together with a realistic scenario. Meet James.

James’s profile:

- Annual gross income: $80,000 ($6,667/month)

- Monthly debts: $350 car loan + $150 student loan = $500/month

- Credit score: 720

- Down payment saved: $25,000 (about 6%)

- Target home price: $400,000

When James submits his application, the lender runs it through an Automated Underwriting System (AUS) — software like Fannie Mae’s Desktop Underwriter® (DU) or Freddie Mac’s Loan Product Advisor® (LPA). The AUS processes everything instantly and returns one of three responses: Approve/Eligible, Refer, or Refer with Caution.

James’s DTI calculation:

- Target PITIA (estimated at 6.8%, 30-yr, with taxes/insurance/PMI): ~$2,850/month

- Back-end DTI: ($2,850 + $500) ÷ $6,667 = 50.2%

At 50.2% back-end DTI, James is right at the edge. A conventional loan with DU approval may approve this — but only if his compensating factors are strong. His 720 FICO® score helps. His 6% down payment hurts.

What happens next:

- If DU returns Refer, James likely needs to reduce his loan amount, pay down debt, or find a co-borrower.

- An FHA loan may be a better fit — FHA’s back-end DTI cap with compensating factors reaches up to 57%.

- With an FHA loan at 3.5% down ($14,000), James preserves more cash reserves — a compensating factor that strengthens his file.

Bottom line for James: His $80,000 salary can realistically support a home in the $320,000–$370,000 range rather than $400,000, unless he reduces other debts or increases his down payment first.

Overcoming Limits with Cash Reserves and Compensating Factors

If your DTI is borderline or your credit score is below ideal, compensating factors can tip the scales in your favor. Think of them as bonus points that offset weaknesses in your application.

The most powerful compensating factors in 2026:

- Substantial cash reserves — having 6–12 months of PITIA in savings after closing is a major underwriting signal

- Low LTV / large down payment — putting down 20%+ removes PMI and reduces lender risk

- High FICO® Score — a 760+ score can offset a slightly high DTI

- Long employment history — 5+ years with the same employer signals income stability

- Minimal payment shock — if your new mortgage is close to what you currently pay in rent, lenders feel more confident

- No outstanding collections or late payments — a clean credit history speaks louder than a high score alone

Strategy tip: If you’re 3–6 months from applying, use that time to pay down credit card balances (improves DTI and FICO® simultaneously) and avoid opening new credit accounts.

How Do Government-Backed Loans Compare to Conventional Mortgages?

Not everyone qualifies — or needs — a conventional conforming loan. Government-backed programs exist specifically for buyers who need a lower barrier to entry.

FHA, VA, and USDA Guidelines Explained

Federal Housing Administration (FHA) Loans

- Min. credit score: 580 (with 3.5% down); 500 (with 10% down)

- Back-end DTI: up to 43–57% with compensating factors

- Down payment: as low as 3.5%

- Caveat: Requires Mortgage Insurance Premium (MIP) for the life of the loan (if down payment < 10%)

Department of Veterans Affairs (VA) Loans

- Eligible: Active military, veterans, surviving spouses

- No minimum credit score set by VA (lenders typically require 580–620)

- No hard DTI cap; uses residual income method

- No down payment required; no PMI

- Funding fee applies (waived for disabled veterans)

USDA Loans

- Eligible: Rural and suburban properties that meet USDA geographic criteria

- Income limits apply (typically 115% of area median income)

- Front-end DTI: 29% | Back-end DTI: 41%

- No down payment required; low mortgage insurance costs

| Feature | Conventional | FHA | VA | USDA |

|---|---|---|---|---|

| Min. Credit Score | 620+ | 500–580 | 580+ (lender) | 640 (typical) |

| Down Payment | 3–20% | 3.5–10% | 0% | 0% |

| DTI Limit | Up to 50% | Up to 57% | No hard cap | 41% |

| Mortgage Insurance | PMI (removable) | MIP (may be permanent) | Funding fee only | Annual fee |

| Loan Limit (2026) | $832,750 | Varies by county | No limit | Varies by area |

PMI vs. MIP: Know the Difference

Private Mortgage Insurance (PMI) applies to conventional loans when your down payment is below 20%. It protects the lender — not you — against default. The good news: once your equity reaches 20% (LTV drops to 80%), you can request PMI removal.

Mortgage Insurance Premium (MIP) applies exclusively to FHA loans. It includes both an upfront premium (1.75% of the loan amount, rolled into the loan) and an annual premium (0.45–1.05%, depending on loan size and term). If you put less than 10% down on an FHA loan, MIP stays for the entire loan term — the only exit is refinancing into a conventional loan later.

This distinction is critical. Over a 30-year FHA loan, MIP can cost $30,000–$50,000 more than comparable PMI on a conventional mortgage.

Frequently Asked Questions (FAQ)

The Equal Credit Opportunity Act (ECOA) requires lenders to evaluate all applicants using strictly financial criteria — income, debts, credit history — regardless of race, gender, religion, or national origin. The following answers apply equally to every applicant under ECOA protections.

What salary do you need for a $400,000 house in 2026?

The income needed depends on your down payment, interest rate, debts, and loan program. With minimal debt, a 6.8% rate, and a 10% down payment on a $400,000 home, your estimated PITIA runs approximately $3,000–$3,200/month. Applying the 28% front-end DTI rule, you’d need a gross monthly income of roughly $10,700–$11,400, or $128,000–$137,000 annually.

With an FHA loan (3.5% down) and a higher DTI tolerance, the salary floor can drop to the $80,000–$100,000 range — but only if your other debts are minimal and your credit profile is strong. Lower existing debt = lower required salary.

What is a good DTI ratio for a home loan?

A back-end DTI of 36% or below is considered excellent — you’ll qualify for virtually any loan program at competitive rates. The 43% threshold is where most lenders draw the practical line; below it, approval is generally straightforward. Between 43–50%, you’ll need strong compensating factors (high credit score, large reserves, or a large down payment). Above 50%, you’re limited to FHA or VA programs, and approval is harder without exceptional compensating factors.

How much deposit is actually required for a mortgage in 2026?

The minimum deposit varies by loan type:

- Conventional: 3% down (Fannie Mae HomeReady® or Home Possible® programs); 20% to avoid PMI

- FHA: 3.5% with a 580+ credit score; 10% with scores between 500–579

- VA: $0 — no down payment required for eligible veterans

- USDA: $0 — no down payment required for qualifying rural properties

Keep in mind that a larger down payment reduces your monthly payment, eliminates PMI, and often qualifies you for a lower interest rate. Even going from 3% to 5% down on a $350,000 home saves you approximately $42/month in PMI — or $5,000+ over 10 years before you’d normally reach 20% equity.

Conclusion: Know Your Number Before You Fall in Love With a House

Understanding how much house loan you can qualify for comes down to five variables working together: your gross income, your existing debts (back-end DTI), your credit score (FICO®), your down payment (LTV), and the loan program you choose.

Here’s your 2026 action checklist:

- Pull your credit report — Check for errors at AnnualCreditReport.com before any lender does

- Calculate your back-end DTI — Add all monthly debts; stay below 43% for the widest options

- Identify your loan program — FHA if credit is below 680; VA if you’re eligible; conventional if you’re above 700

- Check 2026 FHFA limits for your county — Visit fhfa.gov to confirm your conforming loan ceiling

- Get pre-approved — not just pre-qualified — Pre-approval involves real income/asset verification and carries weight with sellers

Ready to see your actual number? Use the Consumer Financial Protection Bureau’s mortgage calculator{rel=”noopener noreferrer” target=”_blank”} to model different scenarios. For official 2026 conforming loan limit data by county, visit the FHFA conforming loan limits page{rel=”noopener noreferrer” target=”_blank”}.

Your dream home is out there. Walk in knowing your number — and you’ll be the most prepared buyer in the room.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage qualification requirements vary by lender, location, and individual financial profile. Consult a licensed mortgage professional for personalized guidance.

By

By