Short answer: No, you can not borrow money from Venmo. There is no loan button, no hidden advance feature, and no payday option inside the app. Venmo is a Peer-to-Peer (P2P) Payment Platform designed to move money between people, not to lend it. But that doesn’t mean you’re stuck — there are legitimate ways to access fast cash inside and outside the Venmo ecosystem, and a few dangerous traps you need to know about before you try anything.

Does Venmo Have a Direct Borrow Feature or Payday Loan Option?

No. Venmo does not have a native borrow feature, a cash advance option, or anything resembling a payday loan inside its Digital Wallet.

Think of Venmo as a digital envelope system: you can put money in, send it to someone, and take it out. It doesn’t create new money for you. The platform is owned by PayPal and is regulated as a money-transmitter service, not as a lending institution. That’s an important legal distinction — lenders must comply with specific federal and state licensing rules, which Venmo simply doesn’t hold.

Some people wonder: “Does Venmo have a Borrow feature like Cash App?” Cash App rolled out a limited Borrow function for select users (amounts between $20 and $200). As of 2026, Venmo has not launched anything equivalent, even in beta. No invite system. No waitlist. Nothing.

If you came here hoping there’s a secret feature — there isn’t. But keep reading, because there are three real options worth understanding.

How Can the Venmo Visa Credit Card Provide Access to Capital?

The Venmo Visa Credit Card is the only native product inside the Venmo ecosystem that technically gives you access to capital you don’t already have. It works like any other Visa credit card — you make purchases on credit and pay them back later.

Who issues it? The card is issued by Synchrony Bank, not by Venmo itself. That matters because Synchrony sets all the terms, fees, and limits — not PayPal or Venmo.

Here’s what the Venmo Visa Credit Card offers:

- A revolving credit line based on your creditworthiness

- Cashback rewards tied to your top spending categories

- Integration with the Venmo app for payment management

Important limitation: The Venmo Visa Credit Card does not permit traditional cash advances at ATMs. Synchrony Bank specifically excludes cash-advance transactions from this card’s terms. Attempts to withdraw cash at an ATM will be declined.

What the card can do is let you make purchases on credit — which, in a pinch, frees up existing cash in your bank account. But it is not a true borrowing product in the way a personal loan or cash advance app would be.

Bottom line: The Venmo Visa Credit Card is a useful everyday card, but it won’t put emergency cash in your hand when you need it most.

What Is the “Credit Card to a Friend” Cash Advance Trap?

Here’s a move many people try when they need quick cash: they link a regular credit card (not the Venmo card) to their Venmo account, send money to a trusted friend, and then ask the friend to send the cash back to their bank account.

It sounds clever. It’s actually a costly mistake.

Why this triggers a Cash Advance classification:

When you fund a Venmo payment using a credit card, Venmo charges you a 3% fee automatically. But that’s just the beginning. Your credit card issuer — Visa, Mastercard, American Express, whoever — sees this transaction as a cash-equivalent transfer. Under their terms, that classifies it as a Cash Advance, not a purchase.

Cash Advances are treated completely differently from regular purchases by every major credit card issuer:

- They carry a separate, higher APR (Annual Percentage Rate — the yearly interest rate on what you owe)

- There is no Grace Period (the interest-free window you normally get before a purchase charges interest). Interest starts on Day 1.

- Your bank adds its own Cash Advance Fee on top of Venmo’s 3% fee

Venmo itself even warns about this on their official help page, noting that some credit card providers may charge cash advance fees when you use your card to make payments to friends.

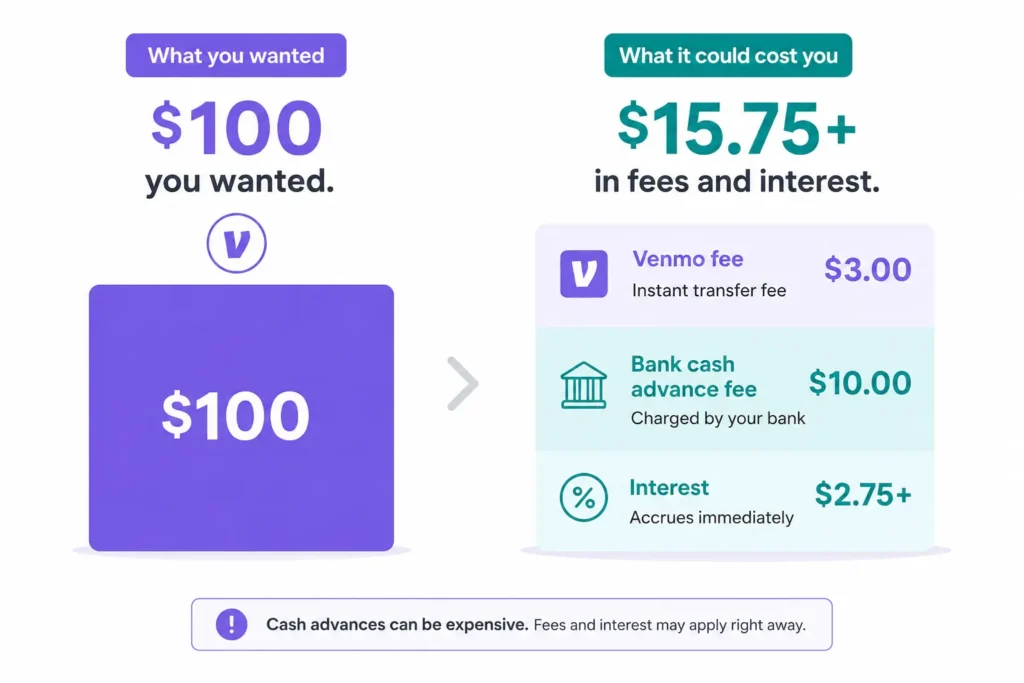

Case Study: The True Cost of Sending a $100 Cash Advance via Venmo

Let’s run the real math on what it costs to “borrow” $100 using a credit card through Venmo.

The scenario: You link your Visa credit card to Venmo. You need $100 in cash. You send $100 to a friend who agrees to immediately transfer it back to your bank account.

Cost breakdown:

| Fee Type | Amount |

|---|---|

| Venmo’s credit card processing fee (3%) | $3.00 |

| Bank Cash Advance Fee (typical: 5%, min $10) | $10.00 |

| Interest on Day 1 at 30.74% APR (daily rate ≈ 0.084%) | $0.09/day |

| Total upfront cost | $13.00 |

| Your friend receives | $100.00 |

| You repay your card | $113.00 + growing daily interest |

Note: The above uses industry-typical cash advance fee figures. Your specific card’s terms will vary — always check your cardholder agreement.

If you take 30 days to repay, add roughly $2.75 in interest on top of the $13 in fees. You borrowed $100 and paid $15.75 for the privilege — an effective APR of around 189%.

For comparison, a traditional personal loan from a credit union typically charges 10–18% APR with no cash advance fees. The Venmo credit card trick is almost always the most expensive possible way to access short-term cash.

The friend also has risks. If Venmo flags the round-trip transaction as suspicious, it can freeze both accounts pending a review. Venmo’s Terms of Service prohibit using the platform to send money for purposes that circumvent standard financial processes.

What Actually Happens If You Force a Negative Balance on Venmo?

Some users wonder: “What if I just spend more than I have in my Venmo balance? Will they cover it?”

Venmo does not allow you to intentionally create a negative balance. Here’s how the system actually works:

Backup Funding Source: When you initiate a payment but don’t have enough in your Venmo balance, the app automatically draws from your designated Backup Funding Source — usually a linked bank account or debit card. You don’t get to skip the payment; Venmo pulls the money from elsewhere.

Negative Balance Protocol: If a transaction fails and results in a negative balance (for example, a payment is reversed after funds were released, or a bank transfer comes back declined), Venmo has a strict recovery process:

- Venmo immediately restricts your account from making new payments

- They attempt to recover the balance from any linked bank account

- Venmo sends collection notices and may charge fees

- If the debt remains unpaid, Venmo may send the balance to a third-party collections agency

That last step matters legally. Once your account goes to collections, the collection activity can be reported to credit bureaus under the Fair Credit Reporting Act (FCRA) — the federal law that governs what information can appear on your credit report. A collections account can remain on your report for up to 7 years and significantly damage your credit score.

The bottom line: Trying to force a Venmo overdraft isn’t a hack — it’s a path toward debt collection and credit damage. It doesn’t work.

What Are the Best Alternative Financial Services for Instant Cash?

Now that we’ve ruled out Venmo as a lending tool, let’s focus on what actually works. The category of apps that provide small, short-term advances is called Alternative Financial Services (AFS) — they fill the gap between payday loans and traditional bank products.

These apps are not unregulated. The Consumer Financial Protection Bureau (CFPB) — the federal agency that protects consumers in financial transactions — oversees this category. Many disclosures these apps make are also governed by the Truth in Lending Act (TILA), which requires lenders to disclose the real cost of credit in plain terms.

That said, AFS apps vary widely in terms of cost, eligibility, and speed. Here’s what you need to know in 2026.

Comparing the Top Cash Advance Apps (Pros & Cons)

The landscape shifted significantly in 2025–2026. Dave eliminated its old optional-tip model and replaced it with a flat fee structure. Empower rebranded as Tilt. The “no mandatory fees” tier is shrinking — EarnIn is now one of the few remaining holdouts.

EarnIn

How it works: EarnIn tracks your actual earned wages (via work email, GPS, or bank activity) and lets you withdraw money you’ve already earned before your official payday.

Pros:

- No mandatory subscription fee

- No mandatory per-advance fee (optional tipping only)

- Up to $1,000 per pay period for established users

- No hard credit check — no impact on your credit score

Cons:

- New users are often capped at $85/day (not the advertised $150)

- Only works for W-2 employees with predictable direct deposits of at least $320/pay period

- Freelancers, gig workers, and 1099 contractors are generally ineligible

- Express “Lightning Speed” delivery fee applies for instant transfers

- Some states (including New York) cap daily withdrawals at $100

Best for: Hourly or salaried W-2 workers who can wait a few hours or overnight for free delivery.

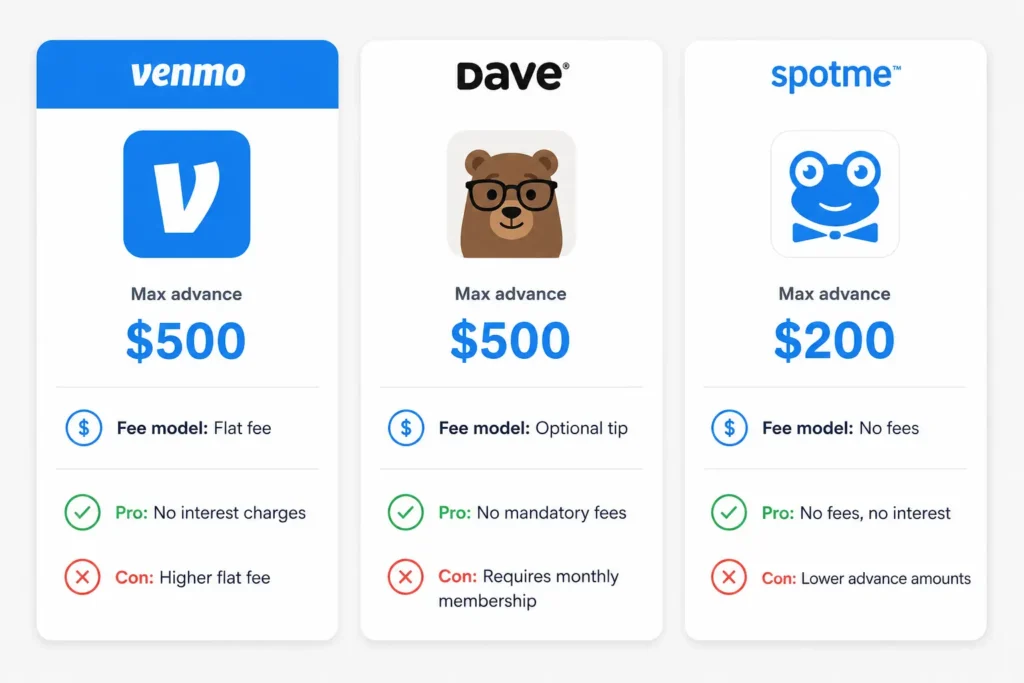

Dave

How it works: Dave’s ExtraCash product advances between $25 and $500 with no interest. After a significant restructuring in 2025, Dave now uses a flat 5% service fee with a $5 minimum and $15 maximum per advance.

Pros:

- Up to $500 per advance

- Flat fee structure is easy to understand

- Instant transfer to Dave Checking is free

- Membership fee capped at $5/month

Cons:

- Mandatory 5% service fee on every advance (minimum $5)

- External bank transfers cost an additional 1.5% fee

- Requires three or more recurring direct deposits totaling at least $1,000/month

- The FTC (Federal Trade Commission) has taken enforcement action against Dave for past fee disclosure issues — a reminder to read the full terms before signing up

Best for: Users who prefer predictable, upfront pricing and are comfortable with a dedicated Dave checking account.

Brigit

How it works: Brigit offers advances from $25 to $500 with no mandatory tipping, a fixed monthly subscription, and no new checking account required.

Pros:

- No tipping model — straightforward pricing

- Includes budgeting tools, credit builder, and overdraft protection

- Standard transfer is free; express fee is $0.99–$3.99

- Works with your existing checking account

Cons:

- Monthly subscription required ($8.99/month)

- New users average about $73 in available advances initially

- Account must be active for 60+ days with three or more recurring direct deposits to qualify

Best for: Users who want a financial wellness app with predictable monthly costs and built-in credit-building tools.

Quick Comparison at a Glance:

EarnIn: Max advance $1,000/pay period | Fee model: Optional tip + Lightning Speed fee | Credit check: No | Gig-worker eligible: No

Dave: Max advance $500 | Fee model: 5% flat fee + $5/mo membership | Credit check: No | Gig-worker eligible: Limited

Brigit: Max advance $500 | Fee model: $8.99/mo subscription + optional express fee | Credit check: No | Gig-worker eligible: Flexible

Are “Free Venmo Money” Hacks and Social Media Lenders Legitimate?

No. They are almost always scams — and they’re becoming more sophisticated.

Here’s the common playbook: Someone on TikTok, Instagram, or X (formerly Twitter) claims to be a “private money flipper” or “Venmo lender.” They promise to send you $200, $500, or more in exchange for a small upfront “deposit” or “verification fee” sent via Venmo first. Once you send your $20 or $50, they vanish.

This is called an advance-fee scam, and it is one of the oldest financial frauds in existence — now repackaged for social media.

The CFPB recognizes this category under Unfair, Deceptive, or Abusive Acts or Practices (UDAAP) — federal consumer protection standards that prohibit financial service providers from misleading or harming consumers. Social media scammers operating this way are not regulated providers at all; they’re criminals.

Warning signs to watch for:

- Anyone asking you to pay money first in order to receive money

- Promises of “no questions asked” loans with no application

- Requests that you pay via Venmo, Cash App, or gift cards (these are not traceable like bank wires)

- Accounts with few followers, no verified identity, and recent account creation dates

- Pressure to act fast (“offer expires in 24 hours”)

Predatory Lending also exists in the formal app store ecosystem. Some apps use deceptive subscription structures that make the effective APR of a small advance equivalent to several hundred percent annually. Before using any cash advance app, search for it on the CFPB’s complaint database at consumerfinance.gov (rel=”noopener noreferrer” target=”_blank”).

If you think you’ve been targeted by a financial scam, you can report it at reportfraud.ftc.gov

Frequently Asked Questions About Venmo and Borrowing

Can you overdraft a Venmo debit card at an ATM?

In most cases, no. The Venmo Debit Card (a Mastercard issued through The Bancorp Bank) does not generally support overdrafts. When you try to withdraw more than your Venmo balance at an ATM, the transaction will decline. If you have a linked bank account set as a Backup Funding Source, Venmo may pull from that account instead — but this is not an overdraft, it’s simply drawing from a linked source. Intentional overdrafts are not a feature Venmo offers.

Will Venmo issue a Form 1099-K if I borrow money from a friend?

It depends entirely on how the transaction is labeled. The IRS Form 1099-K is triggered when you receive payments for goods or services above certain thresholds. For 2026, the reporting threshold is $2,500 in goods/services payments. Personal loans repaid between friends — marked as “personal” transactions — are not classified as income and would not typically generate a 1099-K. However, if you mark a repayment as a payment for goods or services (even accidentally), it may be reported. Always label personal loan repayments clearly in the Venmo memo field and mark them as personal transactions, not business ones.

Does Venmo check your credit score?

Venmo itself does not perform a credit check to open a standard account or use its basic P2P features. However, the Venmo Visa Credit Card issued by Synchrony Bank does require a credit check during the application process — this is a hard inquiry that can temporarily affect your credit score. Cash advance apps like EarnIn and Dave do not perform credit checks. Brigit performs a soft pull only (which does not affect your score).

Conclusion: The Honest 2026 Verdict on Borrowing Through Venmo

Venmo is not a lender, and it was never designed to be one. You cannot borrow money from Venmo directly — no native loan product, no cash advance feature, no beta program exists as of June 2026.

Here’s a quick summary of your real options:

- Venmo Visa Credit Card: Useful for purchases on credit, but does not support ATM cash advances. Apply only if you plan to manage a credit card responsibly.

- Credit card funding trick: Avoid it. The fees stack up fast, and round-trip transactions can get your account flagged.

- Forced negative balance: Impossible and damaging. Don’t try it.

- Cash advance apps: EarnIn (no mandatory fees, W-2 workers only), Dave (flat 5% fee, up to $500), and Brigit (subscription model, most flexible) are your three strongest legitimate options in 2026.

- Social media lenders: Always scams. Report them.

If you need cash today and can’t wait until payday, EarnIn is the lowest-cost starting point for W-2 employees. If you’re a gig worker or freelancer, explore Brigit or Tilt (formerly Empower), which accept more flexible income types.

Before using any financial product, verify current terms directly with the provider — rates and eligibility rules change frequently.

Disclosure: This article is for informational purposes only and does not constitute financial advice. Always review the full terms of any financial product before applying.

borrow money, faqs , easy steps , borrow money from venmo , fee, payment , account , quick , debit card , offer , charge , user , transaction , qualify , review , let you borrow money , quick cash, qualify, review, let you borrow money, quick cash, Can I Borrow Money from Venmo?, Does Venmo Let You Borrow Money?Can You Borrow Money From Venmo

instantly, profile , method , approve , unexpected , bonus , instantly , profile , method , approve , unexpected , bonusmoney instantly, money in your venmo account, solution, venmo user, mobile, arrive, get paid, pay back, amount available, incur, long-term, reduce, venmo also

By

By