If you’re wondering about the best way to invest $1,000 in your 20s in 2026, the short answer is this: cover your financial basics first, then split the money between a tax-advantaged Roth IRA and a low-cost, diversified ETF portfolio. I’ll tell you something: you don’t need to pick winning stocks or time the market. You need a repeatable system, and $1,000 is more than enough to start one.

This guide walks through that system step by step. We’ll cover the prep work, the exact account types to use, how 2026 tax rules can work in your favor, and a real numbers case study so you can see how a $1,000 investment might grow over time.

How Should You Prepare Your Finances Before Investing $1,000?

Before you open a brokerage account, make sure your foundation is solid. Investing $1,000 into the market while carrying high-interest debt is like filling a bucket with a hole in the bottom. Two things need to happen first: pay down expensive debt, and set aside a small safety cushion.

Liquidate High-Interest Debt vs. APY Expectations

Here’s the math that matters. As of mid-2026, the average credit card APR (Annual Percentage Rate) sits close to 24%–25%, according to industry rate trackers. Meanwhile, the long-run average annual return of the U.S. stock market is roughly 8%–10%.

That gap is the whole story. If you carry a $1,000 credit card balance at 24% APR, that debt grows faster than almost any investment could realistically offset. Paying off a 24% APR card is a guaranteed 24% return — no ETF can promise that. So if you have high-interest debt, use your $1,000 (or part of it) to knock it out before investing a single dollar.

- Credit card debt (20%–28% APR): Pay this first, always.

- Student loans (4%–7% APR): Usually fine to invest alongside these.

- Auto loans (6%–9% APR): Case-by-case, but rarely urgent enough to delay investing entirely.

The $500 FDIC-Insured Emergency Fund

Before your money touches the market, build a small buffer — even $500 makes a difference. Keep it in an account insured by the Federal Deposit Insurance Corporation (FDIC), which protects deposits up to $250,000 per depositor, per bank, in the event the bank fails.

This isn’t your full emergency fund (most experts recommend 3–6 months of expenses eventually). It’s a starter buffer so a flat tire or a broken phone doesn’t force you to sell investments early, which can trigger losses and, in some cases, unwanted taxes.

How to Invest $1,000 for Long-Term Wealth in 2026?

Once your foundation is set, it’s time to put your $1,000 to work. For long-term wealth, three moves matter most in 2026: use tax-advantaged accounts first, diversify with fractional shares, and automate future contributions.

Maximize the 2026 Roth IRA Contributions ($7,500 Limit)

A Roth IRA is a retirement account where you contribute after-tax dollars, and your investments grow completely tax-free — you owe nothing on withdrawals in retirement. For 2026, the Internal Revenue Service (IRS) raised the annual contribution limit to $7,500 for people under 50 ($8,600 if you’re 50 or older).

Your eligibility depends on your income. For 2026, single filers can contribute the full amount if their Modified Adjusted Gross Income (MAGI) is under $153,000. Contributions phase out gradually between $153,000 and $168,000, and aren’t allowed above that range. Most people in their 20s fall well below this threshold, which makes the Roth IRA one of the most powerful tools available to a young investor.

Putting your $1,000 into a Roth IRA, invested in a broad index fund, means every dollar of future growth is yours — tax-free, forever.

Build a Three-Fund Portfolio Using Fractional Shares

You don’t need $10,000 to diversify. Most modern brokerages, insured by the Securities Investor Protection Corporation (SIPC) up to $500,000 (including $250,000 for cash), let you buy fractional shares — meaning you can own a slice of an expensive fund for as little as $1.

A classic three-fund portfolio splits your money across three building blocks:

- U.S. total market or S&P 500 fund (roughly 60%): Core domestic growth exposure. Example allocation: $600.

- International stock fund (roughly 25%): Exposure outside the U.S. Example allocation: $250.

- Bond fund (roughly 15%): Stability and lower volatility. Example allocation: $150.

With fractional shares, you can literally split your $1,000 across all three funds in one sitting, regardless of each fund’s per-share price. Many popular index ETFs also carry very low expense ratios — often around 0.03%–0.10% annually — meaning fees eat almost nothing out of your returns.

Automate with Dollar-Cost Averaging (DCA)

Dollar-Cost Averaging (DCA) means investing a fixed amount on a regular schedule, no matter what the market is doing. Setting up an automatic $100/month deposit into a low-expense-ratio S&P 500 Index ETF removes the guesswork — and the anxiety — of trying to time the market.

DCA works because it smooths out your average purchase price over time. Some months you’ll buy at a high point, some months at a low point, and over years those swings average out. This is the strategy that turns a one-time $1,000 investment into a lifelong wealth-building habit.

Where Should You Put $1,000 Right Now for Short-Term Goals?

Not every dollar needs to go into the stock market. If you’ll need this money within the next one to two years — for a move, a car, or a wedding — keep it out of stocks entirely. Short-term investing is really about protecting your money, not growing it aggressively.

High-Yield Savings Accounts (HYSA) vs. CDs

A High-Yield Savings Account (HYSA) is a savings account, usually from an online bank, that pays a much higher interest rate than a traditional bank account. As of mid-2026, top HYSAs are paying around 4.0%–4.2% Annual Percentage Yield (APY), compared to a national average closer to 0.4%–0.6% at traditional banks.

| Feature | HYSA | CD (Certificate of Deposit) |

|---|---|---|

| Liquidity | High — withdraw anytime | Low — locked until maturity |

| Rate | Variable, currently ~4% | Fixed for the term |

| Best for | Emergency funds, near-term goals | Money you won’t touch for a set period |

| FDIC Insured | Yes, up to $250,000 | Yes, up to $250,000 |

If you might need the cash on short notice, a HYSA wins on flexibility. If you know exactly when you’ll need it (say, 12 months from now) and want to lock in today’s rate, a CD can make sense.

How Do 2026 Taxes Impact Your $1,000 Investment?

Most beginner guides skip tax strategy entirely. But understanding a couple of 2026 tax rules can meaningfully change how — and where — you invest your first $1,000.

Leveraging the $49,450 0% Long-Term Capital Gains Rate

Here’s a number almost nobody in their 20s knows about. For 2026, single filers with taxable income up to $49,450 pay 0% federal tax on long-term capital gains (profits from assets held more than one year) and qualified dividends. For context, the 2026 standard deduction for single filers is $16,100, so this 0% bracket applies to a meaningful chunk of income for many entry-level earners.

This is a big deal. If you’re early in your career, a regular taxable brokerage account — not just a retirement account — can be remarkably tax-efficient. You could sell long-term investments and owe nothing in federal capital gains tax, as long as your total taxable income stays under that threshold.

Asset Location Strategies and Form 1040

“Asset location” means deciding which account holds which investment — not to be confused with asset allocation (what you own). A simple rule of thumb:

- Roth IRA: Best for investments you expect to grow the most over decades, since all future growth is tax-free.

- Taxable brokerage account: Fine for index funds you might sell earlier, especially given the 0% capital gains bracket described above.

When tax season comes, your brokerage will send a Form 1099 summarizing dividends and gains, which you’ll report on your Form 1040 (the standard individual income tax return). Roth IRA contributions and qualified withdrawals generally don’t appear as taxable income at all.

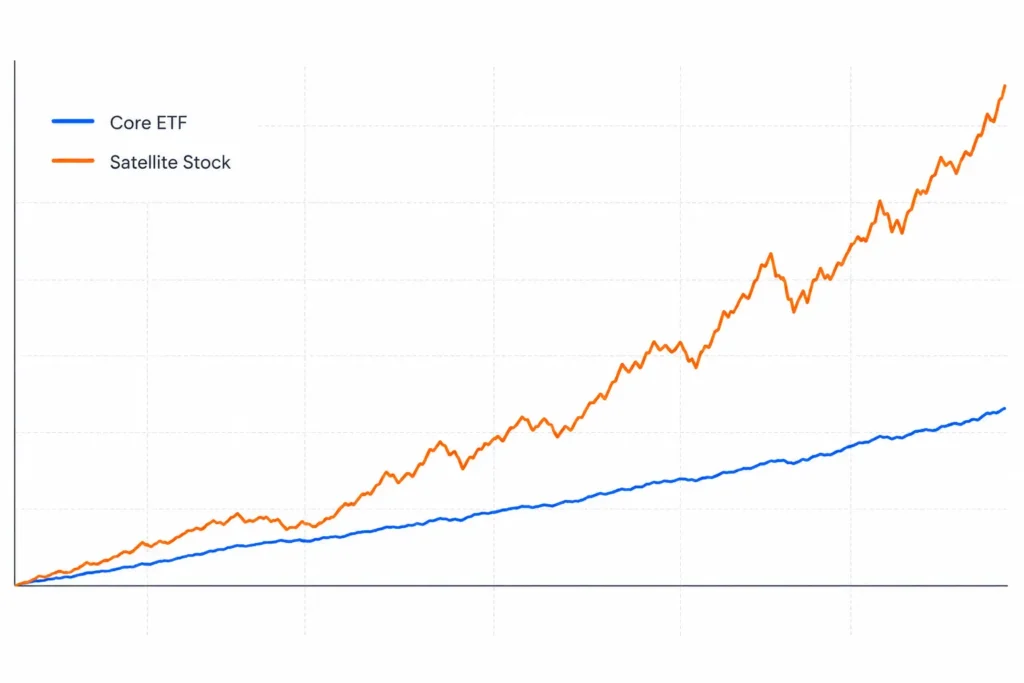

Practical Case Study: The Core and Satellite Approach in Action

Let’s make this concrete. Imagine you invest your $1,000 using a core and satellite strategy: $800 goes into a broad, low-cost S&P 500 ETF (your “core”), and $200 goes into a single higher-growth stock you believe in (your “satellite”).

Calculating Compound Interest (The Rule of 72)

The Rule of 72 is a quick mental-math trick: divide 72 by your expected annual return to estimate how many years it takes your money to double.

- Core ($800 at an assumed 8% average annual return): 72 ÷ 8 = 9 years to double. In roughly 9 years, that $800 could become approximately $1,600, assuming steady average growth (real returns vary year to year).

- Satellite ($200 at an assumed, more volatile 15% average annual return): 72 ÷ 15 = 4.8 years to double. In that same 9-year window, $200 could theoretically double almost twice, reaching roughly $700–$750 — but with far more risk of loss along the way.

Combined, that original $1,000 could grow to somewhere in the $2,300–$2,400 range over 9 years, under these assumptions. This is a simplified illustration, not a guarantee — real markets don’t move in a straight line, and the satellite position carries meaningfully more risk than the core.

[INSERT IMAGE HERE: Simple line chart showing two growth curves — a steady core ETF line and a more volatile satellite stock line — both trending upward over 9 years]

- Alt Text: Core and satellite $1,000 investment growth chart over 9 years

- Title Text: Rule of 72 example: $1,000 core and satellite investing

- Toggle Caption: A steady core position paired with a smaller, higher-risk satellite position.

- AI Generation Prompt: “A clean, modern financial line chart on a white background showing two upward trending lines over a 9-year timeline, one smooth and steady in blue labeled ‘Core ETF’, one more jagged and steep in orange labeled ‘Satellite Stock’, minimalist data visualization style, soft gridlines, no additional text or numbers”

- Technical Specs: 1200 × 800 px, 3:2 ratio, WebP, 80–85% quality, under 150 KB

Pros & Cons: ETFs vs. Individual Stocks with $1,000

Exchange-Traded Funds (ETFs)

- ✅ Instant diversification across hundreds or thousands of companies

- ✅ Lower risk of a single company’s bad news wiping out your investment

- ✅ Typically low expense ratios (often under 0.10%)

- ❌ Growth is usually more moderate — you won’t 10x overnight

- ❌ Less exciting; you’re buying the whole market, not a single “winner”

Individual Stocks

- ✅ Potential for outsized gains if you pick well

- ✅ Full control over exactly what you own

- ❌ High concentration risk — one bad quarter can hurt badly with only $1,000

- ❌ Requires more research and emotional discipline

- ❌ No built-in diversification

For most people starting with $1,000, a core of ETFs with a small satellite of individual stocks (if any) balances growth potential with real diversification.

Frequently Asked Questions

Is $1,000 enough to start investing?

Yes. Thanks to fractional shares, $1,000 is enough to build a genuinely diversified portfolio across U.S. stocks, international stocks, and bonds. You don’t need thousands of dollars per share — brokerages let you buy partial shares for as little as $1, so your $1,000 can be spread across as many funds as you want.

How can I double $1,000 quickly?

There’s no reliable way to double $1,000 “quickly” without taking on serious risk, and most attempts to do so resemble gambling rather than investing. Historically, the stock market has averaged 8%–10% annual returns, which — per the Rule of 72 — means doubling your money takes roughly 7 to 9 years, not weeks or months. Be skeptical of anything promising faster, guaranteed results.

This article is for educational purposes only and does not constitute financial, investment, tax, or legal advice. Money Trail Guide is not a registered investment advisor. Tax figures cited reflect 2026 IRS guidance under Revenue Procedure 2025-32 and are subject to change; consult a licensed financial or tax professional before making investment decisions specific to your situation.

Sources & Further Reading:

- IRS: 401(k) limit increases to $24,500 for 2026, IRA limit increases to $7,500

- FDIC: Deposit Insurance FAQs

- SIPC: What SIPC Protects

By

By